Accountability in the Boardroom 2025

Pension Funds vs.

Equity Index Funds

How Public Pension Funds Managed System-Level Risks Relative to Equity Index Funds

Over 34 million current and former US workers participate in state and local public pension plans, which totaled $4.7 trillion in net assets in 2023.¹ Due to their unique characteristics, public pension funds are among the institutions most exposed to long-lived system-level risks and disruptions. Public pension funds are the quintessential universal owner, as they have broad market exposure through holdings in public equities, private equities, fixed income, and real estate.² Because their portfolios represent the entire market and internalize both positive and negative externalities, public pension funds have a compelling interest in ensuring that our systems serve to bolster economy-wide performance and stability. Defined benefit plans, which comprise the majority of public pension plans, have long investment horizons, are obligated to deliver consistent returns over many decades, and must balance the interests of younger workers with those of older workers and retirees.³

In particular, public pension funds’ obligations to future retirees render them uniquely vulnerable to downside risk.⁴ Funds could fail to meet liabilities towards their beneficiaries and face large penalties if asset values decline and losses compound due to economic shocks, GDP drags, and market underperformance caused by system-level failures. Such a scenario would disproportionately harm Black and women workers, who are more likely to be employed in public sector jobs. Black and women workers are also more dependent on public pension income for retirement security and wealth creation because they have historically been denied access to other channels of asset accumulation.⁵ If workers are forced to absorb pension shortfalls—as happened in Detroit in 2013—due to pension funds’ inability to manage downside risk, this would not only negatively impact middle-class retirement security but also exacerbate existing racial and gender wealth gaps.

Proxy Voting Comparison between Public Pension Funds and Equity Index Funds

Both broad-based equity index funds and public pension funds have considerable exposure to system-level risks by virtue of their long investment horizons and broad-market holdings. Majority Action sought to compare how these two classes of funds approach the problem of mitigating system-level risks through stewardship. To do this, we examined the proxy voting records of the largest public pension funds with respect to our operative universe of shareholder proposals, climate director elections, and say-on-pay votes. We then compared pension funds’ voting outcomes to those of mega and large index funds. We restricted our comparison to mega and large funds because they are commensurate with the largest pension funds in terms of AUM. The largest pension fund in our universe, the California Public Employees’ Retirement System (CalPERS), has approximately $590 billion in assets and is roughly 1.75 times larger than Vanguard’s Institutional Index Fund, the fifth-largest broad-based equity index fund. The smallest pension fund in our universe, the Arizona State Retirement System (ASRS), has approximately $56 billion in assets and is roughly equivalent in size to Nuveen’s Equity Index Fund. Our analysis of shareholder proposals and director elections was restricted to the 17 largest public pension funds where proxy voting data was publicly available, while our analysis of say-on-pay votes included six additional pension funds that are required to disclose compensation-related votes under SEC rules.

Compared to equity index funds, public pension funds were more likely to vote for shareholder proposals addressing system-level issues. Aside from funds in Republican-led states where stewardship decisions are dominated by anti-ESG pressures, the largest pension funds are overwhelmingly supportive of shareholder proposals that confront systemic risks such as climate change, inequality, and unaccountable technology. Interestingly, funds that are leaders on climate and inequality stewardship—such as CalPERS, the New York City Retirement System (NYCRS), Connecticut Retirement Plans and Trust Fund (CRPTF), and New York State Teachers’ Retirement System—somewhat lagged in their support for unaccountable technology proposals. For some funds—such as the Washington State Investment Board and Colorado Public Employees’ Retirement Association—support for unaccountable technology and inequality proposals significantly outweighed support for climate proposals. These varying approaches reflect the relative nascency and emergent terrain of unaccountable technology stewardship.⁶

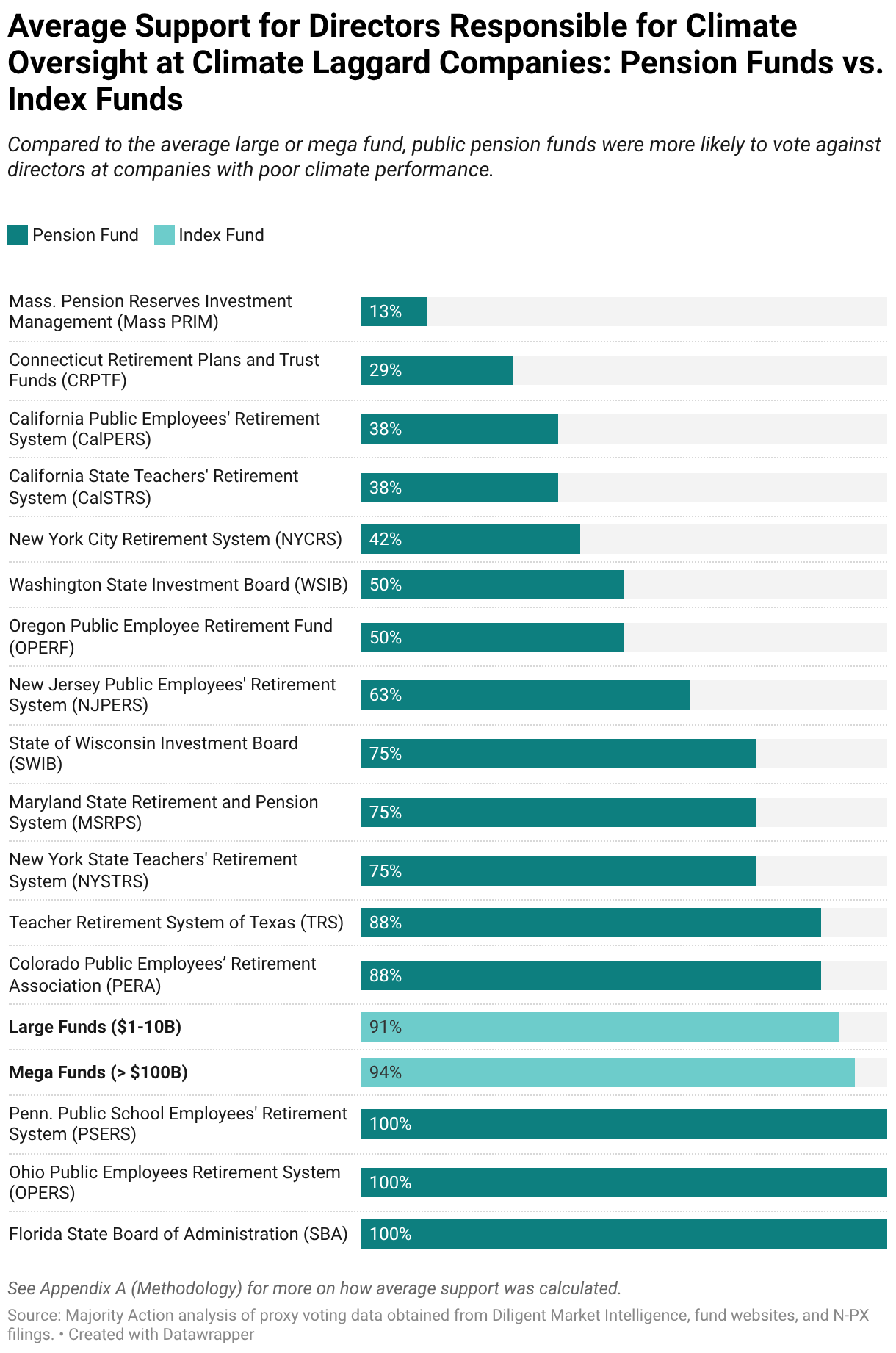

The largest pension funds were also more willing than equity index funds to leverage other proxy voting tools, such as director elections and say-on-pay proposals. 13 out of 16 pension funds outperformed comparable mega and large index funds on director accountability. Massachusetts Pension Reserves Investment Management (MassPRIM), CRPTF, CalPERS, CalSTRs, and NYCRS stood out as leaders in this space, voting against more than half of all responsible directors.

Meanwhile, 20 out of 22 pension funds outperformed comparable index funds on say-on-pay proposals at companies with extreme levels of intra-firm inequality. The Oregon Public Employee Retirement Fund did not support a single say-on-pay proposal. Notably, funds in Florida, Ohio, Texas, and North Carolina—all states impacted by anti-ESG policies and politics—voted against a significant percentage of say-on-pay proposals, suggesting that excessive CEO compensation and intra-firm pay disparities are salient issues that transcend anti-ESG politicians’ chokehold on responsible stewardship.

Finally, Majority Action examined the divergence in proxy voting between pension funds and the ETFs they hold. ETFs constitute a small but growing fraction of public pension fund assets. Public pension plans are reportedly the largest holders of ETFs among institutional asset owners, which collectively held approximately $56 billion in ETFs as of 2023.⁷ Our analysis of 13F filings reveals that the majority of pension funds’ ETF holdings are in funds managed by BlackRock, Vanguard, and State Street.

The chart below shows that many ETFs vote in ways that directly contradict the stewardship priorities of the public pension funds that hold them. The Maryland State Retirement & Pension System (MSRPS) and Florida State Board (SBA) hold $4.2 million and $20.3 million of shares in BlackRock’s iShares Russell 1000 ETF (IWB), respectively.⁸ IWB’s proxy voting on shareholder proposals and director elections diverges significantly from that of MSRPS. Similarly, IWB is far more supportive of say-on-pay proposals at companies with extreme intra-firm inequality (83%) than SBA (28%). Meanwhile, CalPERS holds over $15.9 billion in Vanguard’s S&P 500 ETF, which has long voted against all shareholder resolutions and consistently rubber-stamps management proposals.⁹

Divestment and manager selection are key tenets of responsible investing and system stewardship. Given ETFs’ ease of liquidity and the relative similarity of broad-market index products in terms of investment strategy, portfolio holdings, returns, and fees, pension funds should consider divesting from misaligned BlackRock and Vanguard funds. Instead, they should pool their capital into ETF funds whose proxy voting better align with their investment and stewardship beliefs.