Accountability in the Boardroom 2025

Introduction

The system-level risks posed by climate change, inequality, and unaccountable technology are more salient than ever. Global temperatures are projected to consistently exceed 1.5°C within the next decade, and billion-dollar extreme weather disasters are occurring with increasing frequency.¹ The Trump administration, which has kneecapped domestic investments in clean energy, has engineered a political power grab in Venezuela with the express aim of enriching US oil companies and accelerating extraction of some of the world’s dirtiest oil reserves.² Meanwhile, affordability has emerged as a key concern for working and middle-class Americans who face rising costs, corporate pricing exploitation, a weak labor market, and steep cuts to social safety net programs. There is broad consensus among economists that the pandemic recovery has been “K-shaped,” with gains accruing disproportionately to the top 1% of the income distribution.³ Some analysts have warned that absent AI capital expenditure—which is proceeding at a breakneck pace with little attention to the negative impacts on climate, workers, and democracy—the US economy would be in a recession.⁴

As discussed in previous Majority Action reports, the negative externalities generated by corporations in the form of carbon-intensive business strategies, harmful labor practices, exploitative technologies, and political rent-seeking aggregate into system-level risks that threaten to destroy economic value, hamper economic performance, and destabilize the political, legal, and social systems needed for functional economic and capital markets.⁵ Long-term, diversified investors who hold large swaths of the economy internalize these negative externalities in their portfolios. If unmitigated, climate change, inequality, and unaccountable technology will not only continue to harm our societies, our livelihoods, and our planet, but also erode long-term investment performance. Because these risks are unhedgeable, the only way for diversified investors to decrease their exposure to system-level risks is to mitigate them in the real economy through strategies such as forceful stewardship⁶ and proxy voting.

A Fund-Level Analysis of Proxy Voting

Accountability in the Boardroom examines the 2025 proxy voting performance of the largest asset managers on issues related to climate change, inequality, and unaccountable technology. Most examinations of asset manager voting aggregate votes across all of a manager’s equity-holding funds, overlooking differences in fund characteristics. This approach makes sense, given the centralization of stewardship functions and the fact that most funds in a fund family vote the same way, regardless of fund-specific investment horizons and objectives. Yet in reality, the level of exposure to long-lived system-level risks is different for an alpha-seeking actively managed fund or factor-based growth fund than it is for a Russell 3000 index fund. This report zeroes in on this distinction and looks specifically at asset manager voting from the perspective of one type of fund with considerable exposure to system-level risks: large, diversified index funds that track broad market equity indices.

Broad-market equity index funds track indices that capture vast segments of—or in some cases, nearly the entirety of—the investable equities market.⁷ These funds are often advertised to customers with long investment horizons. The fund website for BlackRock’s iShares Core S&P 500 ETF (IVV), for example, invites prospective investors to “use [IVV] at the core of your portfolio to seek long-term growth.”⁸ Importantly, their low-turnover, buy-and-hold posture means they are effectively locked into the market portfolio and cannot readily exit firms or industries that drive or bear the costs of corporate-driven negative externalities. As a result, their returns depend on the health and stability of the economic system as a whole. These characteristics render broad-market equity index funds especially vulnerable to system-level risks. Given their investment objectives and risk exposure, these types of funds are logical entry points for asset managers to implement system stewardship strategies.⁹

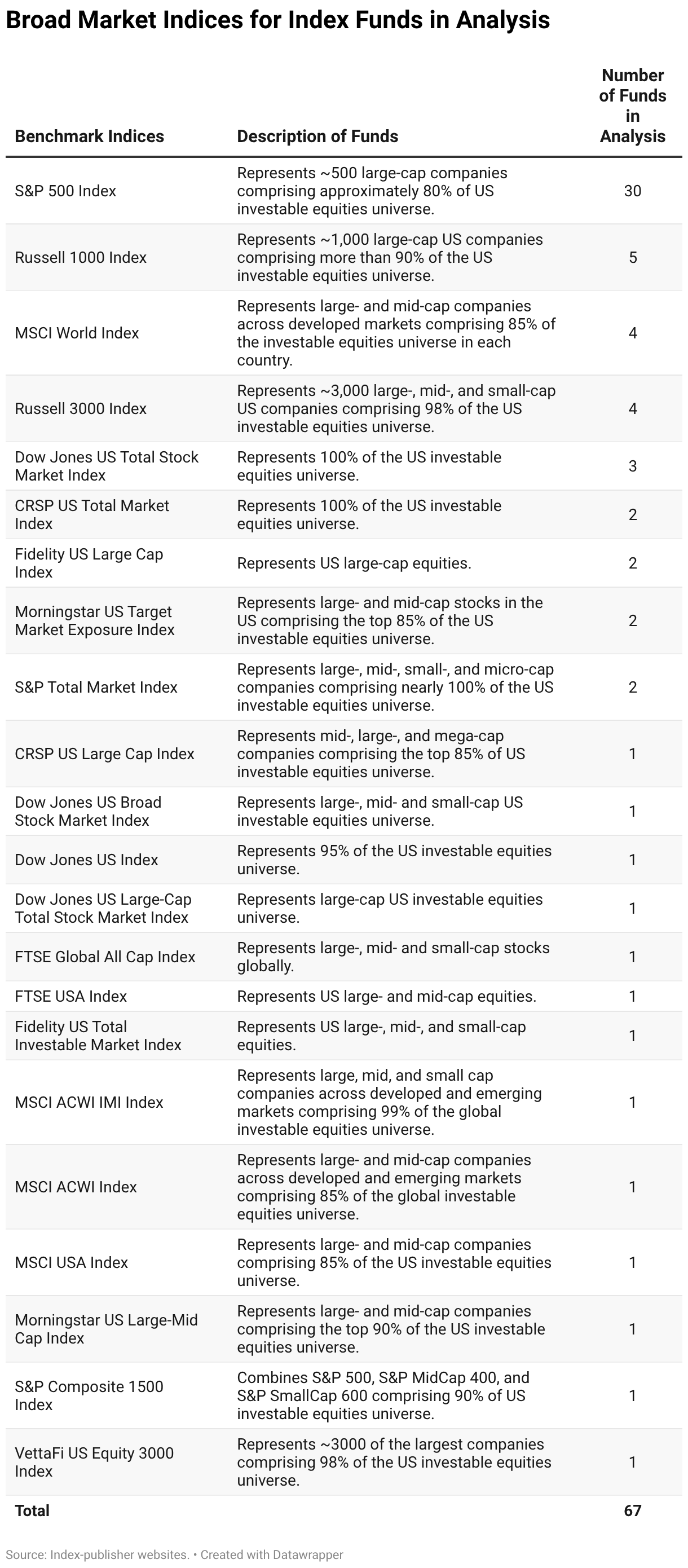

To that end, Accountability in the Boardroom examines the proxy voting records of equity index mutual funds and ETFs with net assets of more than $1 billion that hold US securities and track capitalization-weighted, broad market-diversified indices. In total, we analyzed 67 funds managed by 31 asset managers, totaling $7.4 trillion in assets under management (AUM).

The Unique Role of Mega-Fund Index Managers

While index fund products have proliferated in the past few decades, the broad-based equity index market is highly concentrated and dominated by just five asset managers.¹⁰ Funds managed by BlackRock, Charles Schwab, Fidelity, State Street, and Vanguard account for more than half of the funds in our universe and 95% of AUM. Seven “mega funds”—funds with more than $100 billion in net assets—constitute 83% of AUM.

Big funds are uniquely positioned to shift corporate behavior at scale and mitigate system-level risks through proxy voting. Larger funds command greater voting power across the market. Due to their size and scale, they are less constrained by the cost economics of indexing, enabling them to allocate more resources to stewardship without significantly impacting profits or revenues. Moreover, their broad market footprint—reflected in the sheer number of companies they hold, the large share of the overall market they cover, and the interconnected exposures that come with highly diversified portfolios—enables them to shape governance practices in ways that accumulate into system-level effects. Mega funds, in particular, function as systemically important actors whose voting behavior can shape not only firm-level outcomes but also industry standards and economy-wide externalities. Yet, as our analysis shows, mega funds and their asset managers have effectively abdicated responsibility for mitigating system-level risk through proxy voting. While some smaller funds have emerged as leaders in system stewardship, their ability to change corporate standards and mitigate risks at scale is ultimately limited by virtue of their size.

The Stewardship Failures of Broad-Based Index Funds Put Workers’ Futures at Risk

The failure of broad-based index fund managers to mitigate system-level risks will be felt most acutely by working and middle-class Americans who are saving for a better future. As prominent corporate governance scholar and former Chief Justice of the Delaware Supreme Court Leo Strine notes, the shift from defined benefit plans to defined contribution (DC) plans has transformed workers into “worker-investors” or “forced capitalists,” who must turn a portion of their deferred wages over to mutual funds that are investment options in 401(k), 403(b), and 529 plans in order to save for retirement and pay for college.¹¹ According to the Investment Company Institute, nearly 60% of middle-income households hold mutual funds, and 73% of mutual fund-owning households—including 84% of mutual fund-owning households under the age of 50—hold these funds in employer-sponsored retirement plans.¹² Additionally, 72% of Americans invest in ETFs with the primary goal of saving for retirement, and 59% of Americans own ETFs inside IRAs.¹³ These statistics demonstrate the critical role of these investment products in helping workers secure their financial futures and in strengthening the American middle class.

The diversified index funds examined in Accountability in the Boardroom derive much of their capital from workers’ retirement savings in the form of deferred wages and employer-sponsored contributions. Our fund universe includes low-cost mutual funds that are explicitly designed for and offered as core holdings in DC retirement plan menus, as well as ETFs that are widely held in IRAs. Mega-fund managers—BlackRock, Fidelity, State Street, and Vanguard—play an outsized role in managing workers’ capital because they have successfully secured favored positions within 401(k) and 529 plans.¹⁴ Many of their broad-based index mutual funds are used as the building blocks for 401(k) target date funds and 529 age-based portfolios.

The worker-investors who entrust their capital to these funds are saving for the long-term and hold diversified portfolios that track the entire economy. Their financial security depends on the ability of the economy to generate inclusive and sustainable growth, as well as the willingness of fiduciaries, policymakers, and companies to manage system-level threats that could undermine and upend growth. Moreover, these end-investors are more than just shareholders—they are also wage earners, consumers, and citizens. While they care about the value of their portfolios, most workers save in the hopes of securing a habitable world where they and their children can enjoy stable and dignified employment, a good quality of life, safe consumer products, and democratic rule of law. When the broad-based index fund managers that are most responsible for stewarding retirement capital fail to mitigate system-level risks, they are betraying millions of American workers—undermining not only their portfolio returns, but also the very future they are investing to protect.

Accountability in the Boardroom 2025

Accountability in the Boardroom 2025 is organized as follows. Section 1 examines how the biggest equity index funds voted on shareholder proposals that addressed system-level risks related to climate change, inequality, and unaccountable technology. Section 2 focuses on how funds voted on director elections at eight climate laggard companies spanning the electric utilities, oil and gas, banking, and insurance sectors. Section 3 looks at say-on-pay votes at companies with excessive executive compensation and extreme levels of intra-firm inequality, as measured by the CEO to median worker pay ratio.

Section 4 compares the proxy voting of equity index funds to that of 22 of the largest public pension funds. Like equity index funds, public pension funds have considerable exposure to system-level risks. Public pension funds are the quintessential universal owner and effectively own the entire economy through their holdings in public equities, private equities, fixed-income, and real estate. Defined benefit plans not only have long investment horizons, they must deliver consistent returns over many decades. Public pension funds must also consider the intergenerational implications of their investment and stewardship decisions, since the duty of impartiality requires them to balance the longer-term interests of younger and future workers against the shorter-term interests of current and soon-to-be retirees. In addition to comparing how equity index funds and public pension funds voted on shareholder proposals, climate director votes, and say-on-pay proposals, Section 4 highlights the divergence in proxy voting between public pension funds and the ETFs they hold. Section 5 contains recommendations for asset managers and asset owners to better mitigate the system-level risks related to climate change, inequality, and unaccountable technology.